The internet is obsessed with jamming things into Altoids candy containers. If you placed one of those pocket sized metal tins under a cardboard box leaning on a stick attached to a string, you’d have the perfect geek trap. It’s gotten to the point where you can even buy an empty altoids tin online for the same price as a full one from the grocery store. I assume the selling point is that they’ve already discarded the curiously disgusting mints for you.

A subset of the altoids tin fan club are the survival enthusiasts who compete to create the best pocket survival kit. There are literally hundreds of photos and build instructions for altoids tin survival kits out there. Common things packed are knives, lighters, plastic bags, fishing hooks, duct tape, and paracord. Oddly enough the one thing I never see in these kits happens to be the most useful tool that has ever existed.

I’ll give you a hint

A highly divisible, high density storage of value, and reliable universal medium of exchange. If I had $500 to design the perfect modern survival kit, I would choose 500 $1 bills. Then I could simply buy whatever supplies the specific survival situation called for. I know, I know; the serious preppers would say that you can’t eat money, but I say that if there ever came a time when US currency lost all value you’d be screwed no matter what you stored in the tin anyway.

Keeping a small survival kit and some cash on hand provides an adequate and appropriate degree of protection for likely emergencies. Unless your closest neighbors are farm animals, then going any farther than that is unnecessary. There’s a difference between making a sensible hobby survival kit and keeping a doomsday prepper bug-out van in the garage.

It’s absurd to devote every paycheck to protecting yourself from extraordinarily unlikely events. We currently live in the most peaceful time in history. It makes sense to prepare for hurricanes in Florida, but going into debt to bury guns and canned spam in a bunker is not a logical use of resources.

I converted my 401k into Hot Pockets because you can’t eat money

Unfortunately, they don’t teach money management skills in public schools. And the result is too many people who are financially illiterate and lack an understanding of probability/expected outcome. You’re in for a tough life unless you have smart parents or the opportunity & drive to do the research yourself. I was lucky to have all of the above.

After college I started making more than minimum wage for the first time in my life, and I realized that I needed to get this money management thing figured out while I’m young. I did a lot of reading and eventually discovered the “secret” to personal finance. That money is indeed the ultimate tool, and knowing how to use it will make your life substantially easier. You really don’t have to be an expert to have financial success.

I’ve reached a point now where I’m comfortable moving from the role of student to teacher. I’ve just finished a stack of money related free resources, and I’m sharing them all below. Hope you like them!

.

1. EngineerDog’s New ‘DogPile’ Page: A list of specific tools that provide a high value return in utility or happiness relative to their cost. These are all things that I own or have used and feel 100% comfortable recommending. Are there any specific tools/products that have made a huge positive impact on your life?

. .

2. EngineerDog’s Financial Survival Pocket Guide (PDF): There’s more free financial advice on the internet than you could read in a lifetime. When there’s hundreds of voices clamoring for your attention, the only way to stand out from the crowd is to provide excellent content in a succinct package (Quality > Quantity).

That’s why I’ve created this pocket guide to provide a solid baseline for money management and investing skills. Sure there’s always more tips, subtleties, and minor details to any subject, but this covers the major stuff. Of course I also encourage you to learn from as many different sources as possible, so I’ve recommended some of my favorites at the end of the guide.

.

3. Engineering Economics Calculator (Excel): This is an excel document based on the most common calculations I had to do in my university engineering economics class. This tool can be used to compare two different business investments against each other, or a single investment against the opportunity cost of what your money could have earned in interest elsewhere.

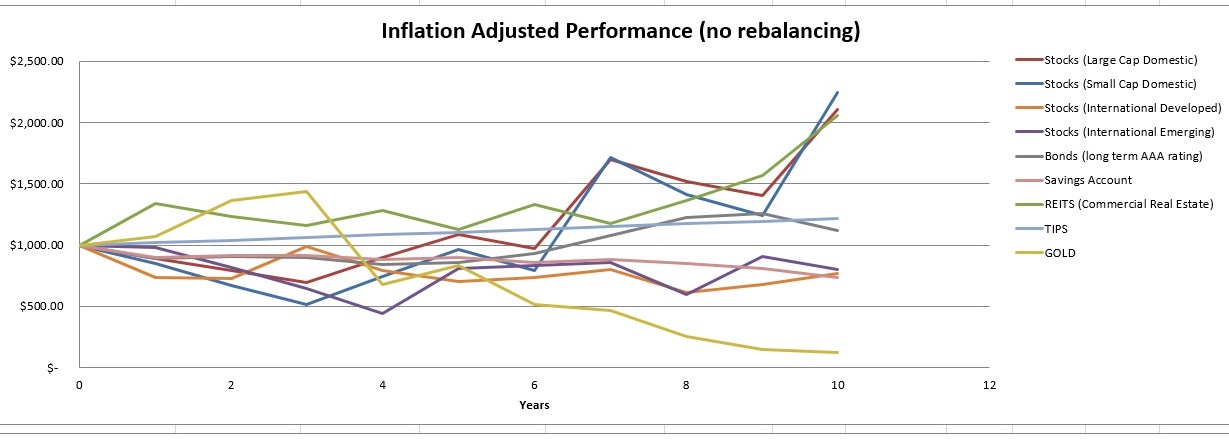

4. Investment Portfolio Performance Tester (Excel): This is a special excel document intended as a pseudo-realistic illustration of how an investment portfolio might perform over time. (This does not predict real stock market performance, but it is based on real data.) The calculator uses your choice of investment time span and your choice of investment allocations to create a graph. All calculations are done twice to compare how your portfolio reacts when rebalanced annually vs being left alone.

4. Investment Portfolio Performance Tester (Excel): This is a special excel document intended as a pseudo-realistic illustration of how an investment portfolio might perform over time. (This does not predict real stock market performance, but it is based on real data.) The calculator uses your choice of investment time span and your choice of investment allocations to create a graph. All calculations are done twice to compare how your portfolio reacts when rebalanced annually vs being left alone.

The realistic aspect of this worksheet is that the numbers it creates aren’t entirely random. It uses data based on the known long term geometric mean and standard deviation of various investment classes. It then creates a set of truly random numbers that conform to the specified mean and std dev.

The specific investment classes are Stocks (Large Cap Domestic, Small Cap Domestic, International Developed, and International Emerging), Bonds (long term AAA rating), Savings Account, REITS (Commercial Real Estate), gold (i.e. my estimate for highly speculative investments), and TIPS (Treasury inflation Protected Securities). The inflation rate is also calculated.

Even though there are 10 asset class variables the worksheet only uses six different sets of randomly generated numbers. Some classes use the same set to create a degree of connection between them while others have their own. This is necessary because it would be nonsense if interest rates and bond values rose at the same time, so they are linked to react inversely. Similarly, the large and small domestic stocks are linked due to their common country & government laws (I.e. small cap would never completely tank relative to large but there would be minor variations between them.) This is all considered for all asset classes.

Remember this is not a perfect model because the results of a given year do affect the others. Past performance does not predict future returns. It is just useful for showing what’s possible.

The result is still entertaining to look at. Every time you press the F9 key (refresh) you can view a different plausible reality. Playing with my model shows that choosing to rebalance annually vs leaving it alone are equally effective. (In real life I ‘rebalance’ actively when I make monthly contributions). The model also shows that diversifying the portfolio by using multiple asset classes instead of just one definitely reduces the risk of losing big. Enjoy the toy!

*PS: EngineerDog is not turning into a personal finance blog, this is likely a one-time thing! Although in my experience engineers do love reading about personal finance. Did you?

**PPS: For those of you not convinced that money is enough of a safety net, I’ve created an instructable on preparing a post apocalypse survivalist hearty camping meal for two. Ha!

For number one, my DeWalt radial arm saw.

LikeLike

Ahh a very versatile woodworking tool! I almost destroyed my hand in one fooling around in highschool woodshop class and they’ve scared me ever since!

LikeLike